Private Equity Ranking: Who's Building, Who's Bleeding, and Why BigLaw May Be PE's Next Acquisition Target

Pirical intelligence data tracking 50,000+ lawyers across PE and capital markets practices reveals a three-year talent reshaping more dramatic than the numbers indicate, and a looming ownership question that BigLaw's most powerful PE advisors are uniquely positioned to answer.

There is a firm that served more than 5,000 publicly tracked private equity matters between 2023 and 2026, deployed nearly 2,800 PE-adjacent lawyers to do it, and still recorded net positive lateral movement in its PE practices. That firm is Kirkland & Ellis. And understanding why Kirkland sits where it does, and what every other firm in this dataset is doing to close the gap, hold ground, or quietly retreat, is the story of how BigLaw's relationship with private equity has fundamentally matured.

Pirical's proprietary platform intelligence, which tracks lawyer movement, headcount, and matter activity across PE and capital markets adjacent practices, captures that story in granular detail. What follows is the most comprehensive data-driven analysis of private equity's imprint on BigLaw yet published, covering matter volume, talent flows, headcount trajectories, practice-level trends, and the regulatory frontier that may soon make law firms themselves the subject of the same ownership calculus their PE clients have applied to every other professional services sector.

Decoding the PE Client Universe

Before mapping which law firms serve private equity best, it is worth being precise about who private equity actually is. Headline AUM figures for the industry's largest managers are deeply misleading as a proxy for legal work. Blackstone manages over $1 trillion in total assets, but the majority sits in real estate and credit; Apollo is primarily a credit firm by AUM. The legal mandates that flow to BigLaw's PE practices (buyout transactions, fund formation, portfolio company work) derive from PE-specific equity portfolios, not the broader platforms.

Pirical has sought to isolate PE-specific AUM across the top 20 managers, stripping out credit, real estate, and infrastructure where segment-level disclosures permit. The resulting ranking differs meaningfully from industry headline figures and provides a more accurate picture of who actually drives the mandates that define BigLaw's PE practices.

Figures reflect PE-specific portfolios; credit, real estate, and infrastructure excluded where disclosed.

Source: PEI 300, disclosed segment data. Figures approximate; Q3 2025.

The Matter Intelligence: Who Is Actually Doing the Work

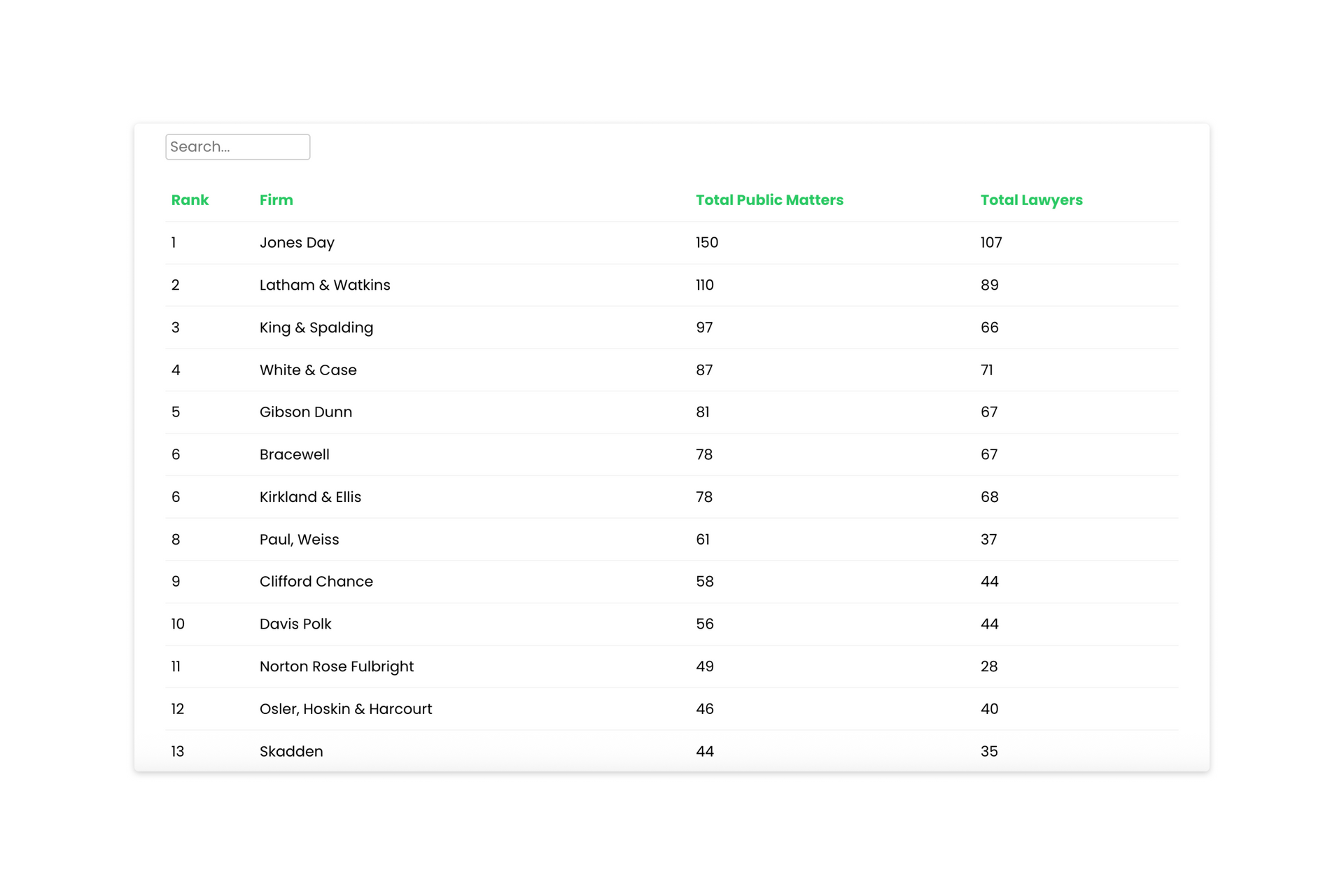

Pirical's matter-level data (cross-referencing publicly disclosed engagements across PE-adjacent practices against the top 20 PE organizations) provides the most granular available picture of which law firms have built durable, high-volume PE relationships. The table below ranks firms by aggregated public PE-adjacent matter count alongside total lawyer deployment. The ratio between the two figures is itself analytically meaningful: a high matter-to-lawyer ratio reflects deal intensity and practice concentration rather than simple headcount scale.

Matters tied to current firm affiliation of lawyers. Practice areas reflect current lawyer designations. Counts reflect unique lawyer-location-matter associations.

Kirkland's dominance is not a surprise, but its magnitude is. At 5,024 tracked matters, K&E produces more than three times the matter volume of its nearest competitor, Latham & Watkins (1,488). The gap between first and second place is larger than the gap between second and twenty-fourth.

Paul, Weiss presents the sharpest matter-intensity ratio in the dataset: 1,088 matters served by 456 lawyers. That concentration reflects the firm's deliberate positioning in high-value, complex PE transactions rather than volume-based market coverage, a strategy whose commercial logic the Barshay-era buildout has validated.

Freshfields at #7 with 910 matters and 581 lawyers is the most significant international firm in the ranking, reflecting both the globalization of PE deal flow and the firm's sustained US practice investment. The presence of Vinge (#19) and Roschier (#22) confirms that Nordic PE (which has produced outsized deal activity relative to market size) is increasingly registering in global matter counts.

Top 10 individual law firm–PE client pairings by public matter count.

The concentration of Kirkland mandates from Francisco Partners, Apax, and Advent reflects the kind of exclusive-channel dynamics increasingly common among the most sophisticated PE buyers. More surprising: Clifford Chance's ranking as the primary legal partner to Partners Group by matter count (appearing above both Ropes & Gray and Latham & Watkins serving the same client) challenges conventional assumptions about which firm wins European PE mandates.

The Talent Wars: Three Years of Movement

Headcount and matter volume reveal market position; lateral movement reveals strategic intent. Pirical's tracking of all lawyer joiners and leavers across PE and capital markets adjacent practices from January 2023 to January 2026 surfaces the clearest picture yet of which firms are genuinely building, which are churning, and which are contracting while managing the optics. The table below combines both columns into a net movement view, a framing that exposes firms whose joiner numbers mask significant underlying instability.

All joiners and leavers across identified PE and capital markets adjacent practices. Net = Joiners minus Leavers. Ranked by net movement.

Simpson Thacher & Bartlett's net +79 is the dataset's most consequential finding. STB has historically been among the most selective and culturally conservative elite PE firms, not known for lateral hiring at scale. 149 joiners against 70 leavers over three years signals a deliberate capacity build, not replacement churn. Paired with a 52% absolute headcount expansion (detailed below), STB appears to be executing a strategic expansion that has received remarkably little market attention.

Goodwin Procter's net -14 tells a very different story. With 88 joiners and 102 leavers, Goodwin was simultaneously recruiting aggressively and losing talent at high volume during a period when its core VC and growth equity market suffered one of its worst multi-year contractions in recent memory. The firm was running a replacement treadmill at precisely the wrong point in the cycle.

Sidley Austin's net -52 is the dataset's most troubling signal for an established PE practice. Sidley is not typically described as a firm people flee, and its PE and funds practices have historically been substantive. 103 departures against 51 joiners over three years points to either systematic poaching by competitors with superior compensation structures (Kirkland and Paul Weiss being the most likely) or internal practice pressures not visible in the public narrative.

Latham & Watkins' net -48 is significant given the firm's matter volume (#2 overall) and brand strength. The combination of high matter activity and meaningful net talent loss could reflect a firm where demand is outpacing its ability to retain the lawyers servicing it, or a firm whose talent is being harvested because of its PE client proximity.

Skadden's net -26 should be read in context: given the firm's historical struggles to hold talent against Kirkland-level compensation pressure, the contained leaver number relative to its market position indicates a degree of stabilization that the conventional narrative underweights.

Absolute Growth: Who Built the Most Capacity

Pirical's three-year tracking of PE-adjacent lawyer populations identifies both the most aggressive capacity builders and the practices that contracted, whether by market force or strategic choice.

Simpson Thacher's 52% growth (from 398 to 605 PE-adjacent lawyers) is the most dramatic documented expansion among elite PE firms in the Pirical dataset. To put the scale in context: STB added more PE-adjacent lawyers in three years than the total current PE-adjacent headcount of Cleary Gottlieb or Fried Frank.

Dentons' -32% contraction and Wilson Sonsini's -30% decline reflect distinct dynamics. Dentons' global verein structure makes its PE practice difficult to assess as a unified entity; the contraction may reflect strategic rationalization as much as genuine client attrition. Wilson Sonsini's decline maps far more directly onto the VC and growth equity market collapse. The firm's identity and geographic concentration left it maximally exposed to precisely the segment that suffered the most severe compression between 2022 and 2025.

Practice-Level Trends: Where the Lawyers Actually Are

Pirical's breakdown across granular practice designations reveals that PE-adjacent legal headcount growth is concentrated in specific areas, and that some practices conventionally assumed to be thriving are in measurable decline.

All lawyers in identified PE and capital markets adjacent practice designations across Pirical dataset.

The divergence between Corporate – Investment Funds (+7%) and Capital Markets – Equity (-6%) is the single most consequential finding in this table. Fund formation has been the most resilient PE-adjacent legal revenue line across this cycle: as PE firms continued to raise successor funds even during lean deployment periods, the lawyers who structure those vehicles held their ground. Equity capital markets work, by contrast, has been directly squeezed by IPO market suppression. The -6% decline in ECM headcount is a precise reflection of deal market reality.

The near-zero aggregate capital markets figure (-0.3%) conceals this split entirely. Analysts who cite flat capital markets headcount as evidence of stability are missing a meaningful divergence within the category.

Geographic Shifts: Where PE Legal Work Is Moving

Pirical's office-level data (filtered to offices with above-average PE-adjacent headcount) identifies the fastest-growing and fastest-contracting markets for this practice cluster.

Growth and decline among offices with above-average PE-adjacent lawyer populations.

Nashville (+42%), Berlin (+31%), Dubai (+30%), and Munich (+28%) reflect distinct but coherent dynamics. Nashville and Austin confirm the migration of PE portfolio companies (and the fund managers that own them) into lower-cost US jurisdictions. Berlin and Munich reflect genuine growth in European PE activity, particularly mid-market buyout activity driven by German Mittelstand succession transactions. Dubai's emergence as a growth office reflects the Gulf's expanding dual role: LP capital source and increasingly active direct investment market.

Hong Kong's -13% contraction (from 895 to 775 PE-adjacent lawyers) is the most consequential geographic finding in the Pirical dataset. Both the absolute scale of the decline and its concentration in PE practices confirms what practitioners have reported anecdotally: geopolitical friction, regulatory uncertainty, and reduced cross-border deal flow between China and Western PE have materially reduced demand for Hong Kong-based PE legal capacity.

The Software Repricing: A Reckoning Flowing Through PE Into BigLaw

Software stocks have clearly entered a bear market in 2026, but the equity selloff may not be the most consequential development. The IGV software index is down more than 23 percent year to date, stock valuations have compressed significantly, and hundreds of billions in market value have evaporated. As recently noted in SaaStr's analysis of the 2026 software downturn, the more systemic risk may sit beneath the equity layer. Private credit funds are estimated to have $600 to $750 billion in exposure to software companies, much of it structured during peak-valuation years. If repayment stress spreads across sponsor-backed portfolios, the consequences extend beyond PE returns. Credit tightening would affect venture debt, growth rounds, and sponsor-led M&A, directly influencing the deal pipeline that sustains BigLaw's private equity and capital markets practices.

The repricing of enterprise software valuations is already a private equity story, and it is beginning to flow into BigLaw.

The IGV software ETF has shed more than 23% year-to-date. Salesforce and Workday are each down over 40% across the past twelve months. Software company valuations have fallen dramatically, with buyer pricing dropping from roughly 30x earnings in 2022 to approximately 16x today, and revenue-based valuations falling from 10-12x to 4x. The cause is not purely sentiment-driven: enterprise CIOs are actively redirecting budgets away from traditional software and toward a $600B+ AI infrastructure buildout, while AI-powered automation is beginning to threaten the subscription-based licensing model that justified a decade of premium valuations.

For PE firms, the practical consequences are severe in ways that will flow directly into legal market demand. Thoma Bravo executed 28 software acquisitions since 2023; Blackstone followed with 24. Many of those transactions were financed at peak valuations. At current valuations, debt payments are increasingly difficult to support; exit windows are frozen; losses are not hypothetical. The posture split is telling: Thoma Bravo and Vista are publicly framing the dislocation as a buying opportunity, while KKR and Apollo are characterizing their software exposure as limited. Goldman Sachs draws the uncomfortable newspaper industry analogy: structural decline dressed as cyclical dip. JPMorgan and Wedbush push back, calling the selloff an overshoot. Both positions can be simultaneously defensible.

For BigLaw's capital markets practices, the downstream effect is real and underappreciated. Frozen exits and refinancing risk mean fewer IPOs, fewer sponsor-to-sponsor transactions, and more restructuring pressure across leveraged software portfolios. Pirical's ECM headcount data (already down 6% across the dataset) may be the leading indicator of a more significant contraction if the software repricing proves structural. Firms like Goodwin, whose VC and growth equity practices were built for a specific market cycle, are most exposed. Firms with diversified PE relationships across sectors (Kirkland, Paul Weiss, Weil) are most insulated.

The Ownership Question: Is BigLaw PE's Next Target?

Private equity has long identified US law firms as one of the last unconsolidated, high-margin professional services sectors: reliable cash flows, low capital intensity, fragmented market, inelastic demand. The obstacle has been singular: ABA Model Rule 5.4, which prohibits fee-sharing between lawyers and non-lawyers, has functionally barred outside equity ownership of law firms across nearly all US jurisdictions. As Berkeley Law's The Network has noted, this same capital wall contributes to the US ranking 109th out of 128 countries in access to affordable civil legal services, giving reformers a powerful access-to-justice argument alongside PE's financial one.

That obstacle is eroding. Arizona eliminated its version of Rule 5.4 in 2021 and now licenses Alternative Business Structures allowing full nonlawyer equity ownership. 136 entities were approved by mid-2025, 59% of which are wholly nonlawyer-owned. Puerto Rico introduced a 49% nonlawyer ownership rule in 2025.

Where outright equity ownership remains prohibited, investors have adapted the Management Services Organization model, borrowed from PE's playbook in healthcare and accounting. The MSO structure separates a law firm's legal practice from its administrative infrastructure, allowing outside investors to own and profit from the latter while the law firm nominally retains exclusive control over legal work. As Sidley Austin's November 2025 analysis details, the MSO's upside is structurally constrained. Investors capture management fees rather than legal revenues, making returns inferior to the accounting firm model where PE has taken direct equity stakes at significant multiples in firms like Grant Thornton and Baker Tilly. Reed Smith's February 2026 market update reports that lenders are now underwriting MSOs based on the durability of long-term management services agreements, with platform acquisitions and multi-firm rollups becoming standard transaction templates.

The Pirical data raises a question that legal market observers have not yet fully engaged: the firms most deeply embedded in PE advisory relationships (Kirkland, Simpson Thacher, Weil, Paul Weiss) are simultaneously the most sophisticated interpreters of PE ownership structures, the most valuable as acquisition targets given their matter volume and client depth, and the most culturally resistant to outside ownership given their partnership-first identity. The legal architects of PE's healthcare rollups and accounting firm investments are now the logical subject of the same playbook.

There is no near-term evidence that any elite firm is actively pursuing or welcoming non-lawyer ownership. But the ABS infrastructure being built in Arizona and the MSO platforms accumulating contractual relationships with smaller firms may be the scaffolding upon which larger-scale consolidation eventually rests, particularly if a major jurisdiction like New York or California moves on Rule 5.4 reform. The medium-term outlook points toward continued incremental state-level reform, MSO platform consolidation, and a horizon within five to seven years where equity ownership in large US law firms becomes a question of corporate strategy, not regulatory theory.

Methodology

This analysis is produced from Pirical's proprietary platform intelligence, which aggregates and structures publicly available and disclosed professional data on lawyers, law firms, matters, and market movement. PE-adjacent practices were identified using Pirical's classification taxonomy, covering Corporate – Private Equity Transactions, Corporate – Investment Funds, Corporate – Investment Funds – PE Funds, Capital Markets, Capital Markets – Equity Capital Markets, and related crossover designations.

Headcount figures reflect January 2023 and January 2026 snapshots. Lateral movement data covers all identified movements within those practice designations between those dates. Matter data reflects publicly disclosed matters and is subject to the following limitations: (1) matters are tied to the current firm affiliation of the lawyers involved; (2) practice areas reflect lawyers' current designations; (3) locations reflect lawyers' current locations; and (4) counts reflect unique lawyer-location-matter associations, not unique matters.

PE-only AUM figures reflect estimates based on disclosed segment breakdowns and fundraise data through Q3 2025. Most firms do not publish granular PE-only AUM consistently; figures should be understood as directionally accurate. Office-level data reflects aggregated headcount filtered to offices above the dataset mean at the January 2023 baseline.

Note on methodology

Source: publicly-available data tracked by Pirical Legal Professionals (PLP)

Timeframe:

Jan 2023 - Jan 2026

Analysis powered by Pirical Legal Professionals (PLP)

Pirical Legal Professionals is the largest attorney database built with the most comprehensive data on the market. Specifically designed for legal recruitment and legal market research.

Pirical seamlessly aggregates data from a wide range of public sources, tracking over 700,000 attorney profiles worldwide. Our data helps law firms source lateral talent quicker, identify candidates with key client relationships, map competitor firm strategies & team structures, and much more.

Subscribe to the latest data insights & blog updates

Fresh, original content for Law Firms and Legal Recruiters interested in data, diversity & inclusion, legal market insights, recruitment, and legal practice management.